Most people never stop to run the numbers. Here’s what happens when you do.

₹1.5 lakh a month. That’s a good salary by any measure. In most Indian cities, it puts you comfortably in the upper-middle class. You can afford your EMIs, feed your family, take a vacation once a year, and still have a little left over.

But “comfortable” and “on track” are very different things. And most people never stop to ask which one they actually are.

Meet Rahul. Age 35. Two kids. ₹1.5 lakh a month. A home loan running. Dreams of a bigger house someday. Good education for the children. Annual family trips. A peaceful retirement, eventually.

Pretty normal life. And yet — when you actually run the numbers — the picture looks a lot more complicated.

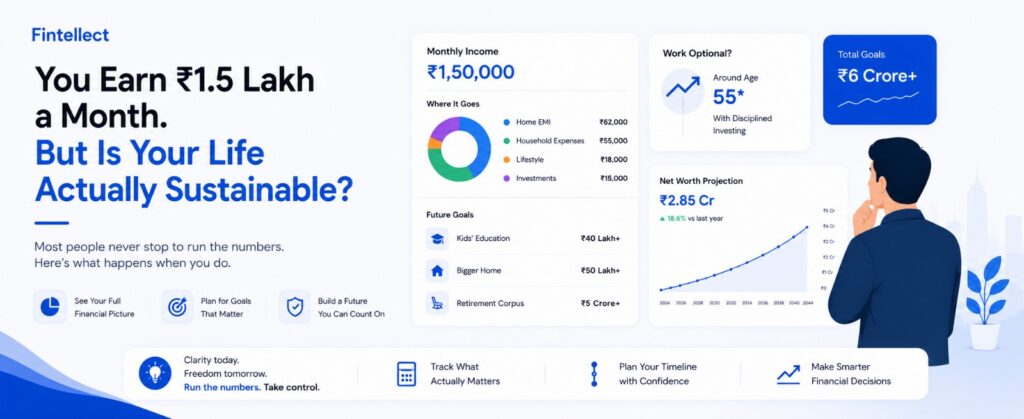

Where the ₹1.5 Lakh Actually Goes

Every month, Rahul’s salary disappears like this:

- Home EMI: ₹62,000

- Household expenses: ₹55,000

- Lifestyle: ₹18,000

- Investments: ~₹15,000

That’s ₹1,50,000. Exactly the salary. Nothing left.

The annual bonus? It disappears into repairs, travel, gadgets, emergencies. There is no “extra.” There is no buffer. The math works — barely as long as nothing goes wrong.

This is what financial life looks like for most Indian professionals. Not irresponsible. Not extravagant. Just… fully committed, with no slack in the system.

The Goals Nobody Has Actually Funded

Here’s where it gets harder. Rahul has life goals the same ones most people his age have. But when you put actual numbers against them, here’s what those goals cost:

- Kids’ higher education: ₹40 lakh

- Bigger home / upgrade: ₹50 lakh

- Parents’ healthcare: ₹20 lakh

- Emergency fund (6 months): ₹9 lakh

- Retirement corpus: ₹5 crore+

Total: somewhere north of ₹6 crore.

At ₹15,000 invested per month which is already everything left after expenses Rahul is investing ₹1.8 lakh per year. Even at a strong 12% CAGR, it takes over 20 years of disciplined investing to cross ₹2 crore. The retirement target alone is out of reach unless something changes.

Salary growth alone may not solve this.

The Question Nobody Asks: When Does Work Become Optional?

There’s a question most people avoid because the honest answer is uncomfortable: at what age will you have enough saved that you could stop working?

Not retire just have the choice.

For Rahul, the math looks like this. If he stays disciplined (investing ₹20K/month, 12% CAGR), he might reach that point around age 55, 20 years from now. If he stays average investing when he remembers, pausing when life gets in the way it’s closer to 30 years. And if he never gets intentional about it, the answer might simply be never.

That’s not a scare tactic. That’s arithmetic.

The Clarity Gap

Here’s the uncomfortable truth about personal finance in India: most people track the wrong things.

Almost everyone knows their monthly income. Most people have a rough sense of their monthly expenses. But almost no one tracks:

- Their future net worth (where they’re actually headed)

- Their obligation timeline (when the big costs hit)

- When work becomes truly optional for them

These are the numbers that actually determine your financial life. And they’re almost never visible.

That gap between what you track and what actually matters that’s the clarity gap. And it’s why people with good salaries still feel financially anxious. They’re flying blind on the numbers that count.

What Running the Numbers Actually Looks Like

The good news is that clarity is not complicated. It doesn’t require a financial advisor or a spreadsheet that takes weeks to build. It just requires actually looking at the full picture income, expenses, goals, timeline, obligations all in one place, and asking the honest questions.

When you do that, decisions change. You stop seeing your EMI as just “the monthly payment” and start seeing it as one piece of a 20-year financial map. You stop treating your bonus as a windfall and start directing it toward the gaps in your plan. You start asking not just “can I afford this?” but “does this get me closer to or further from when work is optional?”

That’s the shift. And it starts with just one thing: running the numbers.

Fintellect is a personal finance clarity platform built for India. Try it free at fintellect.co.in